How to Simply Increase Your Family Wealth by Paying for Housing! By The KCM Crew

Everyone should realize that unless you are living somewhere rent-free, you are paying a mortgage – either yours or your landlord’s. Buying your own home provides you with a form of ‘forced savings’ that allows you to use your monthly housing costs to increase your family’s wealth.

Every month that you pay your mortgage, you are paying off a portion of the debt that you took on to purchase your home. Therefore, you own a little bit more of your home every month in the form of home equity. As your home’s value increases you also gain home equity.

Every quarter, Pulsenomics surveys a nationwide panel of over 100 economists, real estate experts, and investment and market strategists and asks them to project how residential home prices will appreciate over the next five years for their Home Price Expectation Survey (HPES).

The latest data from their Q4 2018 Survey revealed that home prices are expected to round out the year 5.8% higher than they were in January. For the next 5 years, home values will appreciate by an average of nearly 3% a year.

This is still great news for homeowners!

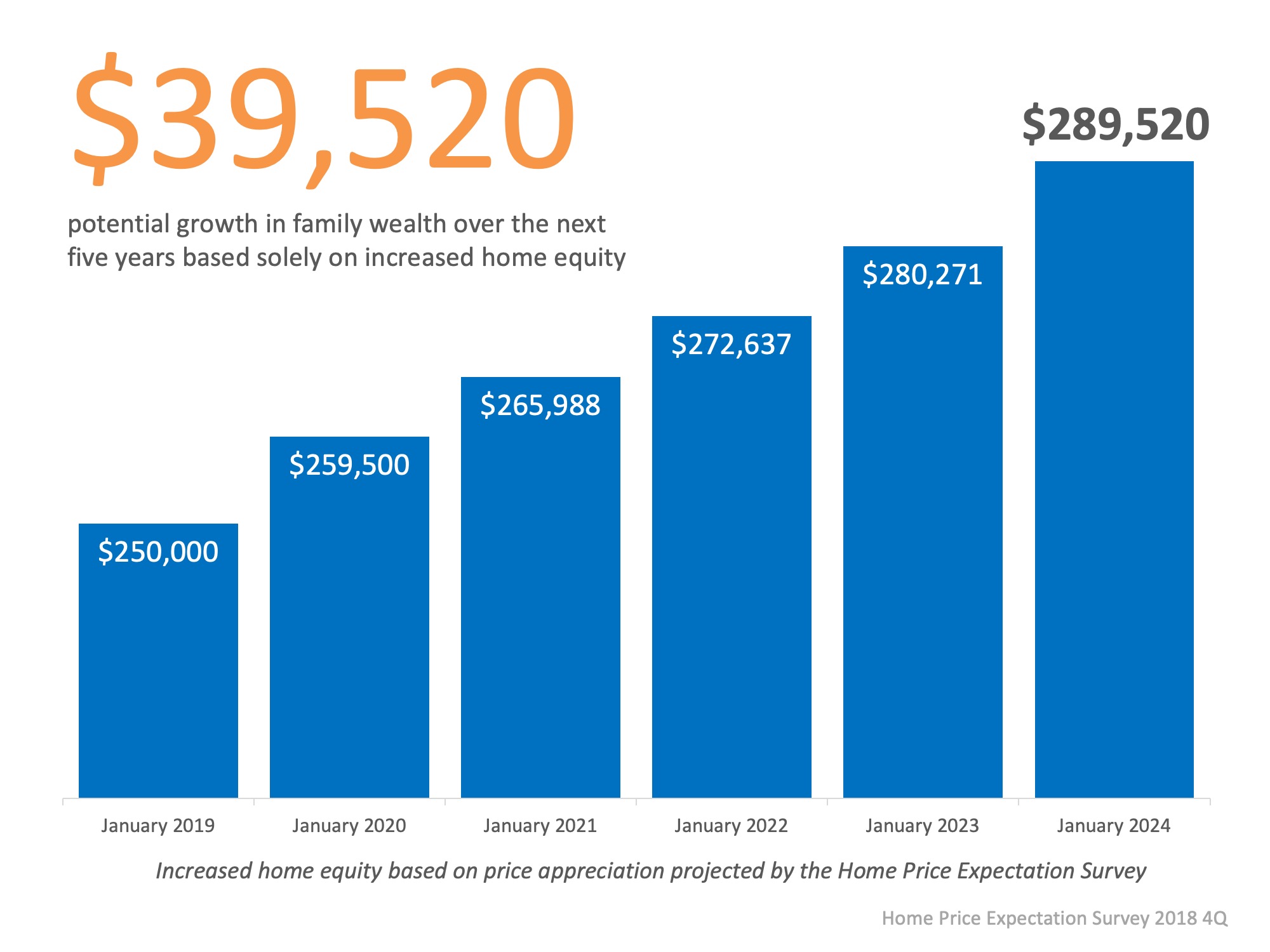

For example, let’s assume a young couple purchases and closes on a $250,000 home in January. Simply through their home appreciating in value, those homeowners can build their home equity by nearly $40,000 over the next five years.

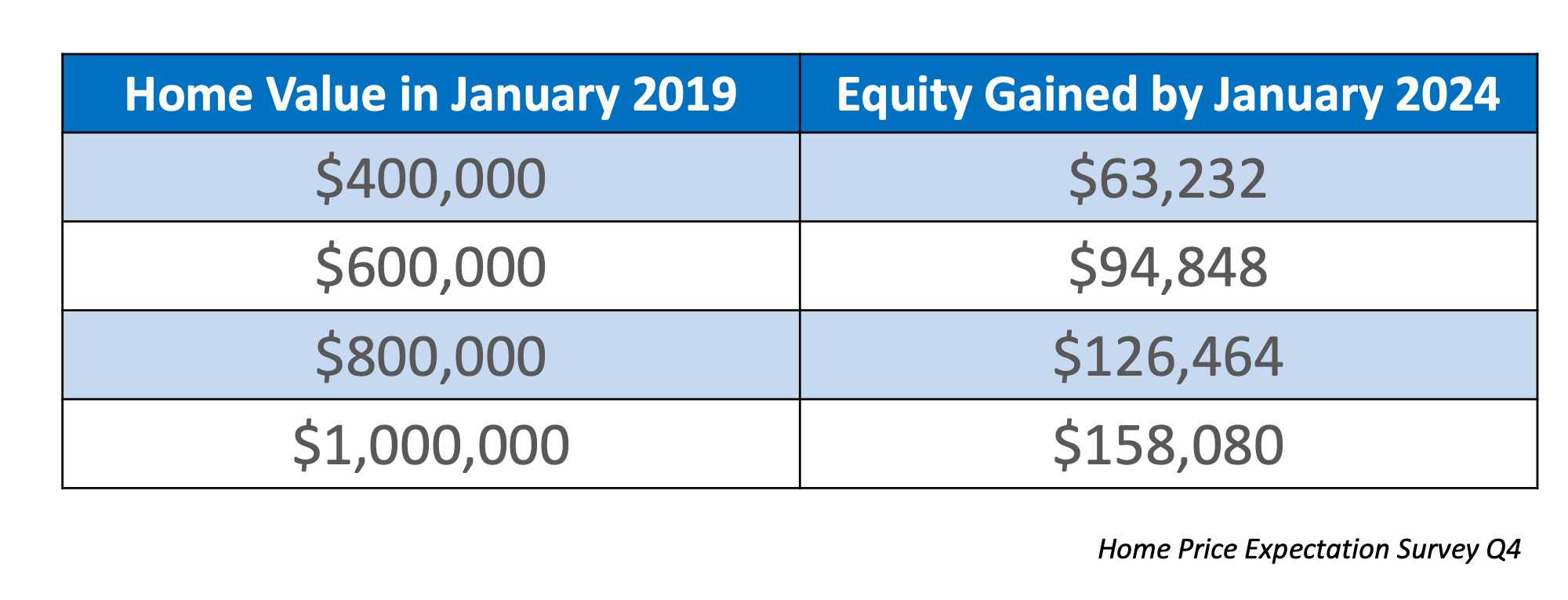

Let’s look at the potential equity gained over the same period of time at some higher price points:

In many cases, home equity is a large portion of a family’s overall net worth.

Bottom Line

If your plan for 2019 includes entering the housing market to purchase a home, whether it’s your first or your fifth, let’s get together to make your plan a reality!